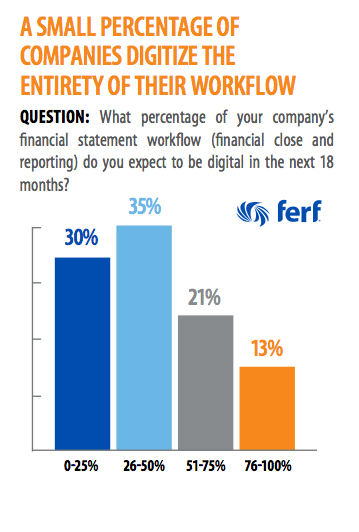

Developing a completely digitized audit workflow remains a challenge for many financial executives implementing an audit structure. A majority of those who responded to the survey that was conducted in 2019 said that they expect less than 50% of their financial statement workflow will be digitized in the next 18 months. Only 13% said they expect 76% - 100% of their workflow to be digital.

“One of the areas we see [many] companies looking at is their financial close process [because] it’s relatively time-consuming in nature and requires a [good amount] of manual effort. So they’re looking at ways in which they can use technologies such as robotics process to [automatically] journal the monthly accrual processes, using that technology to trigger activities in the close [process],” says Scott Szalony, audit & assurance partner with Deloitte & Touche LLP.

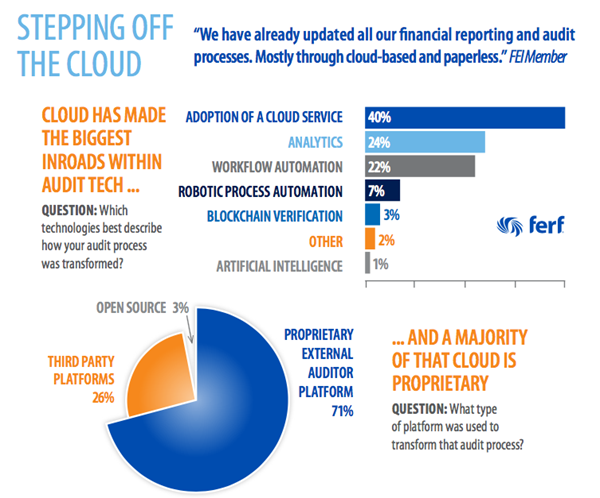

When it comes to actual technology being utilized in today’s audit and financial reporting processes, cloud-based systems represent the largest percentage, according to the FERF survey.

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. In the United States, Deloitte refers to one or more of the US member firms of DTTL, their related entities that operate using the “Deloitte” name in the United States and their respective affiliates. Certain services may not be available to attest clients under the rules and regulations of public accounting. Please see www.deloitte.com/about to learn more about our global network of member firms.